Why "Good" Businesses Fail to Sell: 5 Silent Value Killers Hiding in Your Diligence

- Founders Links

- Jan 27

- 4 min read

Updated: May 2

The Diligence Paradox: From Partner to Interrogator

Most mid-market deals do not collapse because the business is fundamentally flawed. They fail because during the high-stakes due diligence window, the buyer uncovers risks they hadn’t priced into the initial Letter of Intent (LOI).

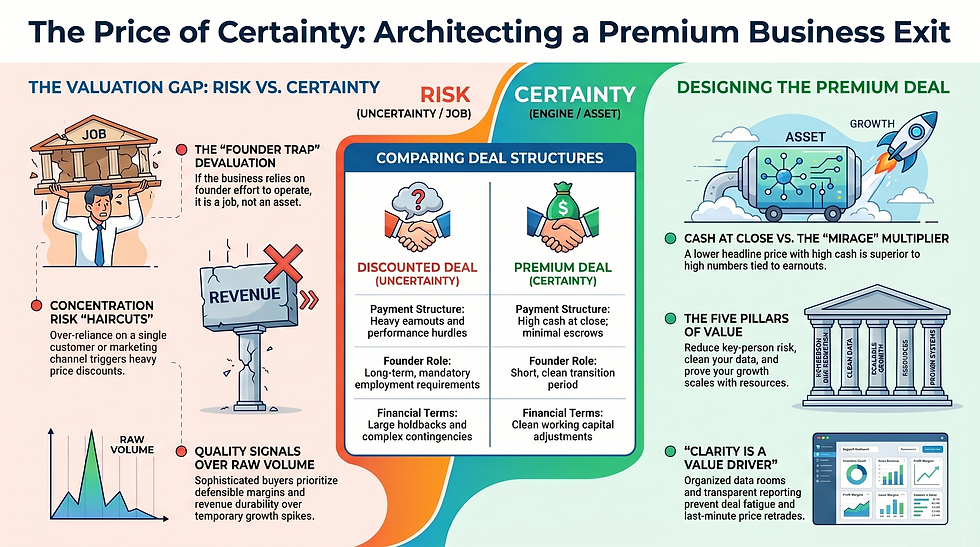

This is the Diligence Paradox: You have built a high-performing company, yet the moment an undocumented risk surfaces, the buyer’s psychology shifts instantly. They move from an enthusiastic "partner" seeking growth to a sceptical "interrogator" seeking reasons to hedge their bets. When trust erodes, momentum dies. The result is rarely an immediate exit; instead, the buyer protects their downside by demanding aggressive price reductions, heavy earnouts, or punitive holdbacks. To secure a premium exit, you must neutralise these five value killers before the first data room is opened.

Value Killer #1: Customer Concentration and Weak Contract Protection

Revenue concentration is the most visible "red flag" in M&A. When a handful of clients represent a significant percentage of your top line, the buyer views your business as fragile. This perception is exacerbated when contracts are short-term, informal, or "relationship-based." While a founder might see a handshake agreement as a sign of trust, a buyer sees it as a lack of contractual rigour that could evaporate the day after closing.

"Buyers price the downside: if one customer leaves, the whole model changes. Even if the relationship is strong, the risk is expensive."

Immediate Remediation:

Quantify the Exposure: Audit your top 5 and top 10 customers to determine exact revenue percentages and historical volatility.

Codify the Commitment: Transition informal agreements into formal contracts with clear terms regarding renewals, pricing escalators, and restrictive termination clauses.

Execute a Diversification Playbook: If concentration is high, prioritise a sales sprint to broaden the customer base, ensuring no single entity holds the keys to your solvency.

Value Killer #2: The Hero’s Tax (Founder Dependency)

In M&A, the "Hero’s Tax" is a direct deduction from your purchase price. If you are the primary driver of sales, the owner of critical client relationships, or the sole "product brain," you are a single point of failure. From a buyer’s perspective, every hour the founder spends in the "engine room" is an hour they must eventually pay a high-priced executive to replace.

This key-person risk directly impacts the buyer’s Internal Rate of Return (IRR). To mitigate this, they shift the deal value away from upfront cash and into "structure"—long-term earnouts and retention packages that force you to stay. A business that requires "heroic involvement" is a job; a business that runs on systems is an asset.

Strategic Fixes:

Institutionalise Relationships: Methodically transition key account ownership from the founder to a professionalised account management team.

Install a Second Line of Leadership: Empower a layer of management capable of making autonomous decisions across sales, operations, and delivery.

Standardise the "How": Document core processes so that results are the product of the system, not the individual.

Value Killer #3: Financial "Fog" and Opaque Reporting

Inconsistent reporting and convoluted segmentation create a "financial fog" that suggests a lack of control. When margins fluctuate without a clear narrative or revenue recognition is aggressive, it triggers a psychological barrier. If your numbers cannot survive a "stress test" against a cynical buyer’s perspective, the buyer will automatically assume the risk is higher than reported.

"When buyers can’t trust the numbers, they assume risk is higher. That often means lower valuation and tighter terms."

The M&A Playbook:

Eradicate Opacity: Tighten the monthly reporting cadence to ensure absolute consistency across all financial statements.

Defend Your Add-Backs: Ensure every "Owner's Add-Back" is documented with forensic-level evidence. If you can't prove it, a buyer will ignore it.

Segment for Clarity: Clean up revenue and cost data by product line, region, and customer type to demonstrate exactly where the profit is generated.

Pre-Diligence Readiness: Compile a "diligence-ready" financial pack that anticipates the interrogator’s questions before they are asked.

Value Killer #4: The Illusion of Growth (Revenue Quality)

Buyers do not pay for last month’s revenue; they pay for the statistical probability that it will continue and grow. "Lumpy" revenue or growth driven by heavy discounting is a major red flag—it suggests the product cannot win on its own merits and that you are effectively "buying" revenue to inflate your valuation. High-quality revenue is durable, predictable, and highly likely to recur.

Operational Hygiene:

Measure the Leakage: Implement rigorous churn tracking and, more importantly, document the specific reasons why customers leave.

Define "Premium Revenue": Prioritise high-margin, long-term contracts over "lumpy" one-off deals that distort your growth profile.

Professionalise the Pipeline: Enforce CRM discipline, track win/loss ratios, and ensure your growth isn't reliant on a single, non-repeatable channel.

Value Killer #5: Legal Landmines and Documentation Gaps

Technical hygiene is often overlooked until it’s too late. Legal risk is notoriously difficult to quantify, which makes it dangerous. Missing contracts, unclear Intellectual Property (IP) ownership (particularly with contractors), or inconsistent employee agreements create unquantifiable liabilities. In these cases, buyers don't just ask for a discount; they protect themselves with massive holdbacks or indemnities—or they simply walk away.

Risk Mitigation Sweep:

Standardise the Legal Stack: Consolidate and standardise all key customer and vendor contracts to ensure they are signed and stored centrally.

Secure the IP Fortress: Explicitly fix IP assignment language in all contractor agreements to ensure the company owns 100% of its intellectual assets.

Audit Employment Gaps: Ensure employee agreements and non-competes are consistent and enforceable (where enforceable under local jurisdictions, such as California or international territories).

Corporate Cleanliness: Validate the cap table and ensure all shareholder resolutions are accurate and signed.

Conclusion: From "Value Killer" to "Roadmap"

Most value killers are not existential flaws. They are fixable operational gaps that require time, focus, and a strategic lens. By identifying these "discounts" early, you gain the leverage to demand a better valuation, cleaner terms, and a significantly faster path to closing.

60-Second Self-Check If you are planning an exit or recapitalisation in the next 12–24 months, ask yourself:

Could we lose our top customer and still look stable?

Can the business run for 60 days without the founder in the room?

Are our numbers clean enough to defend under cynical scrutiny?

Is our revenue repeatable, or just recently strong?

Would we be calm if diligence started next week?

If any of these questions create discomfort, do not view it as a failure of your leadership. Instead, recognise that this discomfort is your roadmap. Addressing these gaps is the fundamental difference between owning a business and owning an asset you can sell.

Comments