Why Two Identical Businesses Sell for Different Prices: The Hidden Mechanics of Deal Value

- Founders Links

- Jan 27

- 4 min read

Updated: May 2

Founders are frequently seduced by the "revenue multiple." They scan industry reports, see a competitor sold for 6x, and assume their business is entitled to the same. In the reality of the M&A trenches, that number is a vanity metric until the buyer’s clinical assessment is complete.

A sophisticated acquirer doesn’t start with a math problem; they start with a risk assessment. They aren’t asking how much revenue you have, but rather: "How confident am I that this performance will continue, without surprises, after the wire hits your account?" Valuation, at its core, is simply the price of certainty.

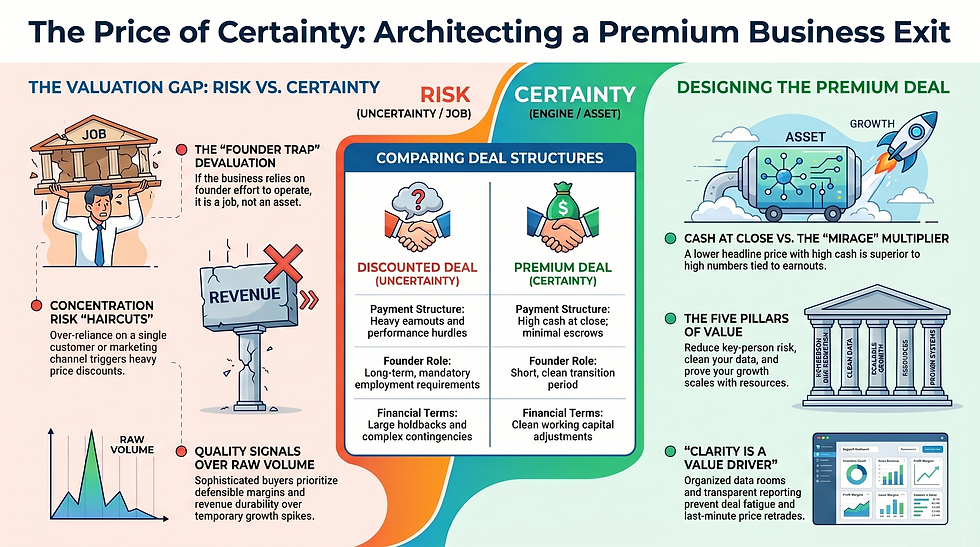

Takeaway 1: Buyers' Price Confidence, Not Just Cash Flow

Two companies can show identical EBITDA on a T12 basis yet receive offers that are worlds apart. This gap exists because buyers prioritise durability, transferability, and risk over raw volume. They are looking for "quality signals", specifically margins, to prove that your revenue is defensible and real, not just a temporary spike driven by unsustainable pricing.

"Premiums come from what reduces risk and increases upside. Discounts come from what creates uncertainty."

A premium is a fee the buyer pays for a business that will survive the transition of ownership. If the story doesn't match the data, or if the margins are opaque, the buyer will protect themselves by shifting the risk back to the seller through a lower price or aggressive deal structures.

Takeaway 2: The "Founder Trap" (If You Are the Engine, You Are the Risk)

One of the most brutal valuation levers is founder dependency. If the business relies on "heroic founder effort" to close deals or manage operations, it is inherently fragile. A buyer is looking to acquire a self-sustaining engine, not a high-pressure job that forces them to hire the founder indefinitely just to keep the lights on.

To achieve a transferable business, you must build a leadership bench and documented processes that ensure the team, not the individual, manages the customer. If you are the primary engine of the business, the buyer isn't buying a company; they are buying a person. The irony of the exit is that the more indispensable you feel, the less your business is actually worth.

Takeaway 3: The "Easier to Buy" Premium

Clarity is a value driver. Professional buyers are deterred by "messy books" and the "we’ll explain that later" adjustments that plague disorganised deals. When a business is "easy to buy," it creates a momentum in diligence that protects the headline price and increases deal speed.

Confidence is built through consistent monthly reporting and a well-organised data room that provides clear segmentation by product, region, and customer. When the data is believable, and the reporting is clean, you eliminate the "deal fatigue" that often leads to last-minute price retrades.

Takeaway 4: The Invisible Weight of Concentration Risk

Even a high-growth business will face a significant "haircut" if it is top-heavy. Concentration risk isn't just about having a single dominant customer or supplier; it also includes dependence on a single marketing or distribution channel. If 90% of your leads come from one platform, you are one algorithm change away from insolvency.

Buyers price in the downside of these dependencies, even when current performance is at an all-time high. This risk usually manifests in the deal terms: lower multiples, heavy earnouts, or "wait-and-see" structures where the buyer refuses to pay full price until they are certain the model won't break after the sale.

Takeaway 5: Premium is a Measure of Certainty, Not Just Price

Founders often obsess over the headline valuation on a Letter of Intent, but a high number is a mirage if the terms are toxic. A true "Premium Deal" is characterised by high cash at close and clean terms, whereas a "Discounted Deal" is a minefield of contingencies designed to protect the buyer from the seller’s risks.

A Premium Deal: High cash at close, minimal escrows, clean working capital adjustments, and limited warranties and indemnities.

A Discounted Deal: Heavy earnouts, performance hurdles, seller notes, large holdbacks, and long-term founder transition requirements.

A $10 million offer with $9 million in cash at close is almost always superior to a $12 million headline number that requires three years of gruelling performance hurdles and a massive indemnity escrow.

Takeaway 6: The Strategy of Removing Discounts

The most effective path to a premium valuation is to stop chasing higher multiples and start removing the factors that cause discounts. By systematically eliminating the reasons a buyer would say "no," you naturally move toward a premium outcome. This also makes the business "eligible" to strategic buyers willing to pay for synergies they can capture immediately.

Focus on these five pillars of the "Founder Links" approach:

Reduce key-person risk: Ensure the business runs without you.

Strengthen data readiness: Maintain clean, segmented, and believable financial reporting.

Improve revenue durability: Focus on repeat usage, contracts, and healthy margins.

Clarify the growth engine: Prove the business scales with resources, not just founder hours.

Create competitive interest: Run a structured process that gives you leverage.

Conclusion: Leverage is the Ultimate Goal

The ultimate goal of M&A preparation is leverage. When you remove risk, improve transferability, and provide clear data, you give the buyer fewer reasons to hedge their bets. Leverage is what drives competitive interest and forces buyers to pay for the "upside" they hope to capture.

As you evaluate your operations, ask yourself a cold, unsentimental question: Is your business an "engine" that you happen to own, or are you the engine itself? If it's the latter, the check you receive at closing isn't a windfall; it’s just a pre-paid salary for a job you aren't allowed to quit.

Comments