Beyond the Spreadsheet: The 5 Counter-Intuitive Truths About How Buyers Actually Price Your Company

- Founders Links

- Jan 27

- 4 min read

Updated: May 2

We have seen $100M deals collapse under the weight of a single customer contract, even as the founder was still in the weeds, obsessively tweaking the terminal growth rate in cell Z104 of their spreadsheet. Many entrepreneurs operate under a persistent "Founder’s Myth": that valuation is a mathematical certainty, a fixed number waiting to be discovered at the bottom of a perfectly crafted Discounted Cash Flow (DCF) model. In the air-conditioned vacuum of a spreadsheet, the logic is flawless. But in the trenches of M&A, valuation is a messy, high-stakes negotiation shaped by market forces, buyer-specific logic, and the perceived weight of risk. To secure a premium exit, you must stop polishing the model and start understanding the strategic mechanics of how buyers actually move their money.

1. Truth #1: Your DCF is a “Check,” Not the Driver

Founders often spend weeks agonising over discount rates, yet sophisticated buyers rarely use a DCF as their primary pricing engine. In mid-market M&A, the DCF is a "reasonableness check", a tool used post hoc to justify a price that was already determined by market comparables and pro forma adjustments. The real pricing mechanism is a dynamic formula: Base Price ± (Premiums and Discounts). Buyers start with an anchor multiple of EBITDA or ARR based on what similar businesses are trading for, but they don’t stop there. They care less about your projected spreadsheet and more about the fundamental levers that drive the multiple: your growth rate, margin profile, retention/churn, revenue visibility, and competitive position. “In real M&A, valuation is not a single number from a spreadsheet. It’s a negotiation shaped by three forces: Market pricing (what comparable businesses are trading for), Buyer logic (what this asset is worth to them), and Risk (how much uncertainty the buyer must absorb)."

2. Truth #2: The “Same” Company Has Multiple Prices

A fundamental reality of the market is that your company does not have one "true" value. Because of Strategic Value, the exact same asset is worth significantly more to a buyer who can use it to transform their own P&L. While a financial buyer might offer a standard market multiple, a strategic acquirer is looking for "upside" they can’t build themselves. Buyers pay a "strategic premium" when the acquisition provides specific levers to accelerate their own growth. These triggers include:

● Cross-selling opportunities: Unlocking the buyer’s existing customer base for your product.

● Geographic expansion: Instant entry into a locked market.

● Product gap fulfilment: Completing a buyer's product suite faster than their R&D team can.

● Churn reduction: Increasing "stickiness" by bundling your solution.

● Competitive removal: Consolidating market share and pricing power.

● Talent and capability: Acquiring a specialised team or IP that is difficult to replicate.

3. Truth #3: Buyers’ Price Probabilities, Not Forecasts

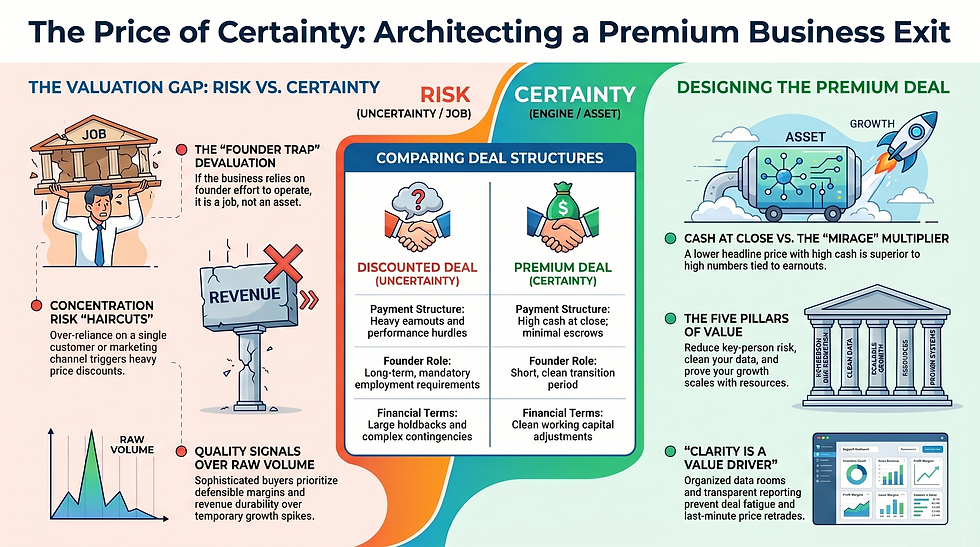

Founders sell the future, but buyers price the probability of that future materialising. This is the essence of "Risk Pricing." A buyer may agree that your cash flow is impressive today, but they will aggressively discount it if they perceive execution risk or a lack of durability. They aren’t just looking at your bottom line; they are auditing your unit economics, specifically your Gross Margin, CAC, and Payback periods, to see if your growth is repeatable. To avoid a valuation "haircut," you must eliminate the "Diligence Landmines" that signal uncertainty:

● Customer Concentration: If a single client’s departure can cripple your performance, the buyer prices in that risk immediately.

● Messy Financials: Unreliable reporting leads to "deal fatigue" and higher perceived risk, causing buyers to claw back value.

● Revenue Quality: One-off revenue is vanity; buyers pay for contractual visibility and diversified revenue streams.

● Compliance Gaps: IP ownership disputes or unresolved legal threats are the fastest ways to kill a premium.

4. Truth #4: The “Founder Trap” is Your Biggest Valuation Leak

A business that cannot operate without its founder is a job, not an asset. "Founder Dependency" is perhaps the most common detractor from value. If you are the primary rainmaker, the sole product visionary, or the essential operational glue, the buyer isn't buying a company; they are buying a person. This creates massive key-person risk, leading to a lower price or more aggressive earnout terms. To command a premium, you must prove the business is a self-sustaining machine. This requires "second-line leadership," documented processes, and a systematised sales motion that functions independently of your personal charisma. If the company’s success is tethered to your daily presence, your valuation has a hard ceiling.

5. Truth #5: Headline Multiples are Vanity; Structure is Reality

Founders love to brag about "10x multiples", but the headline number on a term sheet is often a mirage. In M&A, valuation is a combination of price and risk allocation. Two deals with identical valuations can yield vastly different outcomes depending on their structure and the "certainty of proceeds”. A $50M headline price with a 50% earnout is not a $50M win; it is a $25M bet on your own future labour under someone else's management. Buyers use structural components to hedge their bets, including:

● Earnouts and Performance Conditions: Tying payments to future milestones.

● Working Capital Adjustments: Tweaking the final price based on the assets left in the business at closing.

● Escrows and Holdbacks: Retaining funds to cover potential liabilities.

● Seller Notes: Converting a portion of your exit into a loan to the buyer.

● Non-competes and Role Expectations: Mandating your continued involvement and restricting your future moves. The tension in any deal lies here: the higher the headline price, the more structural "hooks" a buyer will likely insert to protect their downside.

Conclusion: Building Value by Removing Discounts

Securing a premium exit requires a radical shift in mindset. Instead of spending your energy on financial engineering in a spreadsheet, focus on improving the business today by systematically removing the factors that cause buyers to discount your price. The goal is to build options, whether that leads to a full exit, a recapitalisation, or partial liquidity on founder-friendly terms. By diversifying your customer base, institutionalising your sales process, and cleaning up your data, you create a business characterised by durable performance and repeatable growth.

Closing Thought: Buyers don't pay for forecasts; they pay for the evidence that the forecast will come true. Are you offering them a durable, de-risked company, or just a story they don't believe in?

Comments